This article was originally published by Tyler Durden at ZeroHedge.

Update (0800ET Monday, Oct. 3rd): Traders have woken up this morning to more systemic fragility as Credit Suisse debt and equity is dumped in an unceremonious rejection of the CEO’s letter of reassurance over the weekend.

Who could have seen that coming?

JT Marlin has pulled the offer https://t.co/vTnKEPQVwv

— zerohedge (@zerohedge) October 3, 2022

CS stock is down over 5% in pre-market trading (ADRs) to a new record low…

Update: <4CHF, $10BN https://t.co/8gvjRdZYoO

— zerohedge (@zerohedge) October 3, 2022

And CS credit risk has spiked to record highs this morning, topping 280bps at one point – basically disallowing the company from any investment banking business. This is higher than the bank’s credit risk traded at the peak of the Lehman crisis…

While the credit default swap levels are still far from distressed and are part of a broad market selloff, they signify deteriorating perceptions of creditworthiness for the scandal-hit bank in the current environment. There is now a roughly 23% chance the bank defaults on its bonds within 5 years.

The relationship between debt risk, equity price (lower price, less asset value to cover debt, higher credit risk), and equity risk (higher equity risk, higher asset risk, higher credit risk) is a complex one – but one that nevertheless is tradable, by so-called capital structure arbitrageurs. The chart above shows a simple ‘implied spread’ derived from the company’s equity price and volatility. As can be seen, it is well below the current spread trading in professional markets.

This means one or more of these three things: the credit risk premium in the market is too high, the equity price is too high, and/or the equity volatility is too low.

Take your pick.

We note that during a carefully worded and defensive segment this morning on CNBC, they cited sources as saying Credit Suisse’s liquidity position is strong.

Additionally, several market participants (and freshly minted experts in CDS that seemed to suddenly appear on Reddit) sought to dismiss the moves. However, we do note that infamous credit arbitrageur Boaz Weinstein did speak up too, suggesting there was scaremongery afoot…

Oh my, this feels like a concerted effort at scaremongering. See my recent tweets. In 2011-2012 Morgan Stanley CDS was twice as wide as Credit Suisse is today. Take a deep breath guys. https://t.co/mEr2rPsCDP

— boaz weinstein (@boazweinstein) October 1, 2022

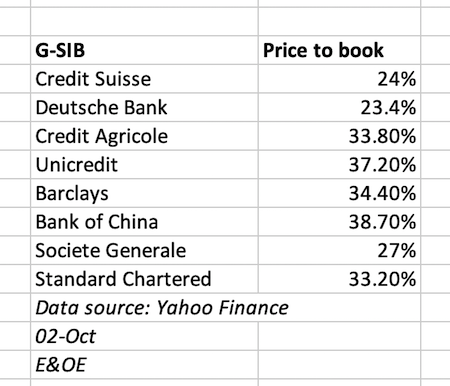

Finally, it is worth mentioning, as Alasdair Macleod recently pointed out, Credit Suisse is not the only major bank whose price-to-book is flashing warning signals.

This list shows all G-SIBs with Price-to-Books of under 40%. A failure of one of them is likely to call the survival of the others into question.

Trade accordingly.

* * *

For the second straight week, Credit Suisse’s new CEO Ulrich Koerner sought to reassure investors (and in fact all global market participants) that the troubled Swiss bank is ‘safe’.

While conceding that there is a lot of uncertainty and speculation both within and outside the bank, the CEO said the bank is at a “critical moment” as it prepares for its latest overhaul.

Koerner told employees not to confuse the “day-to-day” stock price performance with the Swiss firm’s “strong capital base and liquidity position.”

The market – simply put – does not believe him as the credit markets are pricing in the chance of default at its highest level since the peak of the Great Financial Crisis…

And it appears counterparties to the bank’s derivatives transactions are aggressively hedging their exposure to the Swiss bank’s possible failure to perform…

The bank – which has been hit with a corporate spying scandal, a record trading loss, shuttered investment funds and a deluge of lawsuits in recent years – is due to announce a major new strategic plan on Oct. 27 and as we recently noted has said that reports of a ‘bad bank’ split off to hold its high-risk (read low-quality) assets are “categorically false.”

In August, Deutsche Bank analysts predicted that paring back the investment bank while growing other business lines and strengthening its capital rations would leave a US$4bn hole in the group’s capital position.

“Running down other parts of the investment bank and selling smaller businesses across divisions could help over time, but this would likely come too late to avoid an equity raise,” wrote Deutsche analysts Benjamin Goy and Sharath Kumar Ramanathan.

As Bloomberg reports, Credit Suisse’s market capitalization dropped to around 10 billion Swiss francs ($10.1 billion), meaning any share sale would be highly dilutive to longtime holders.

The market value was above 30 billion francs as recently as March 2021.

Credit Suisse executives have noted that the firm’s 13.5% CET1 capital ratio on June 30 was in the middle of the planned range of 13% to 14% for 2022.

The firm’s 2021 annual report said that its international regulatory minimum ratio was 8%, while Swiss authorities required a higher level of about 10%.

Creditor Suisse pic.twitter.com/vmbnY36Imt

— zerohedge (@zerohedge) September 29, 2022

So CS has a “strong capital base and liquidity position”? Like reports that “Bear Stearns was not in trouble”, “Lehman is well capitalized”, and “subprime was contained”?

Finally, as Larry MacDonald writes at The Bear Traps Report: Credit Suisse is NO Lehman, but it´s on par with Bear Stearns.

“We are well capitalized” comments from Alan Schwartz and Ulrich Koerner are 14 years apart but ominously appear nearly identical.

Must not forget, stocks puked lower into the Bear Stearns rescue and rallied 23% (NDX) on the follow. It is time to connect the dots – we now have Paul Krugman, Jeremy Siegel very publicly chastising Powell, and Harvard´s Greg Mankiw writing an opinion piece screaming, the Fed has indeed overcooked the Porter House. Oh, by the way, our favorite Fed pawn, Timiraos was sharing Mankiw´s sentiment early Sunday morning. Hmmm.

It all comes down to risk-weighted assets.

When Lehman and Bear failed, their core capital – U.S. Treasuries – were NOT dropping like a stone. In the last twenty years, our global banking system has NEVER faced a one-two punch of interest rate risk and credit risk combined.

Can you imagine being a board member of Credit Suisse? You take the Archegos and Greensill financial hits – then come war, an energy crisis-driven recession, and your foundation bedrock capital on the balance sheet, good old government bonds are dropping 10-30 points in a month. The CET1 ratio compares a bank’s capital against its assets. Additional Tier 1 capital is composed of instruments that are not common equity. In the event of a crisis, equity is taken first from Tier 1. It´s a measurement of a bank’s core equity capital, compared with its total risk-weighted assets.

With the declines in government bonds in Europe coupled with near certain recession risk – bank balance sheets look more like Credit “Swiss Cheese” than strong financial institutions.

0 Comments