This article was originally published by Charles Hugh Smith at Of Two Minds Blog.

The value of these super-abundant follies will trend rapidly to zero once margin calls and other bits of reality drastically reduce demand.

Inflation, deflation, stagflation–they’ve all got proponents. But who’s going to be right? The difficulty here is that supply and demand are dynamic and so there are always things going up in price that haven’t changed materially (and are therefore not worth the higher cost) and other things dropping in price even though they haven’t changed materially.

So proponents of inflation and deflation can always offer examples supporting their case. The stagflationist camp is delighted to offer a compromise case: yes, there are both deflationary and inflationary dynamics, and what we have is the worst of both worlds: stagnant growth and declining purchasing power.

What’s missing in most of these debates is a comparison of scale: deflationists point to things like big-screen TV prices dropping. OK, fine: we save $300 on a TV that we might buy once every two or three years. So we save $100 a year thanks to this deflation.

Meanwhile, on the inflationary side, healthcare insurance went up $3,000 a year, childcare went up $3,000 a year, rent (or property taxes) went up $3,000 a year, and care for an elderly parent went up $3,000 a year: that’s $12,000. Now how many big-screen TVs, shoddy jeans, etc. that dropped a bit in price will we have to buy to offset $12,000 in higher costs?

This is the problem with abstractions like statistics: TVs dropped 20% in cost, while healthcare, childcare, assisted living and rent all went up 20%–so these all balance out, right?

There are two glaring omissions in all the back-and-forth on inflation and deflation:

1. Price is set on the margins.

2. Enterprises cannot lose money for very long and so they close down.

Let’s start with an observation about the dynamics of price/cost: supply and demand. As a general rule, things that are scarce and in high demand will go up in price, and things that are abundant and in low demand will drop in price.

Whatever is chronically scarce and necessary for life will have a ceaseless pressure to cost more, whatever is abundant and no longer desirable will have a ceaseless pressure to cost less.

Now we come to the overlooked mechanism #1: Price is set on the margins. Housing offers an example: take a neighborhood of 100 homes. The five sales last year were all around $600,000, and so appraisers set the value of the other 95 homes at $600,000.

Things change and the next sale is at $450,000. This is dismissed as an outlier, but then the next two sales are also well below $500,000. By the fifth sale at $450,000, the value of each of the 95 homes that did not change hands has been reset to $450,000. The five houses that traded hands set the price of the 95 houses that didn’t change hands. Price is set on the margins.

The biggest expense in many enterprises and agencies is labor. Those who own enterprises know that it’s not just the wage being paid that matters, it’s the labor overhead: the benefits, insurance and taxes paid on every employee. These are often 50% or more of the wages being paid. These labor overhead expenses have skyrocketed for many enterprises and agencies, increasing their labor costs in ways that are hidden from the employees and public.

It’s important to recall that roughly 3/4 of all local government expenses are for labor and labor overhead–healthcare, pensions, etc. Where do you think local taxes are heading as labor and labor-overhead costs rise? What happens to pension funds when all the speculative bubbles all pop?

The cost of labor is also set on the margins. The wage of the 100-person workforce is set by the five most recent hires, and if wages went up 20% to secure those employees, the cost of the labor of the other 95 workers also went up 20%. (Employers can hide a mismatch but not for long, and such deception will alienate the 95% who are getting paid less for doing the same work.)

Labor is scarce for fundamental reasons that aren’t going away:

1. Demographics: large generation is retiring, replacements are not guaranteed.

2. Catch-up: labor’s share of the economy has declined for 45 years. Now it’s catch-up time.

3. Cultural shift in values: Antiwork, slow living, FIRE–all are manifestations of a profound cultural shift away from working for decades to pay debts and enrich billionaires to downshifting expenses and expectations in favor of leisure and agency (control of one’s work and life).

4. Long Covid and other chronic health issues: whether anyone cares to admit it or not, Long Covid is real and poorly tracked. A host of other chronic health issues resulting from overwork, stress and unhealthy lifestyles are also poorly tracked. All these reduce the supply of labor.

5. Competing demands of family and work. Work has won for 45 years, now family is pushing back.

Put these together–diminishing supply of labor and labor being priced on the margins–and you get a runaway freight train of higher labor costs. Add in runaway increases in labor overhead and you’ve got a runaway freight train with the throttle jammed to 11.

Deflationists make one fatally unrealistic assumption: that enterprises facing sharply higher costs for labor, components, shipping, taxes, etc. will continue making big-screen TVs, shoddy jeans, etc. even as the price the products and services fetch plummets below the costs of producing them.

The wholesale price of the TV can’t drop below production and shipping costs for very long. Then the manufacturers close down production and the over-abundance of TVs, etc. goes away. Nation-states can subsidize production of some things for a time, but selling at a loss is not a long-term winning strategy: subsidizing failing enterprises and money-losing state-owned companies is a form of malinvestment that bleeds the economy dry.

The only thing that will still be super-abundant as demand plummets is phantom-wealth “investments”, i.e. skims, scams, bubbles and frauds. The value of these super-abundant follies will trend rapidly to zero once margin calls and other bits of reality drastically reduce demand.

Real-world costs: much higher. Speculative gambles: much lower. As in zero.

Thank you, everyone who dropped a hard-earned coin in my begging bowl this week–you bolster my hope and refuel my spirits.

A combination of government spending of borrowed money into the general economy combined with a tax rate too low to remove it from the economy and stabilize money supply in relation to overall production causes inflation.

Not in this case. Bidenflation is the direct result of leftist supply chain sabotage resulting in roughly the same amount of dollars or less chasing artificially reduced supply.

U.S. dollar printing goes directly into financial instruments, tied up for years generating small amounts of interest. Some trickles back into the real economy of goods and services.

Vented excess dollars happens regularly in things like stock market corrections and assorted bad investments and popped bubbles.

Taxes are already too high and an ineffectual solution to inflation even if the rich were taxed. The super rich, aren’t numerous enough to impact middle class inflation.

Its not like the run on private luxury jets affects the average consumer.

They just want that stimulus money back

Money for nothin and your chicks are free is an urban myth…

A while ago a worthy over at ZeroHedge went back through all the incidences of hyperinflation (currency collapse) all the way back to the time of the Roman Empire with startling conclusions.

Two factors alone set the stage for economic calamity those being the Total Money in circulation tandems with the Velocity of Money. In ALL cases, when both were pronounced, then hyperinflation followed invariably.

Thre total money in circulation (roughly equivalent to M1) is currently at stratospheric levels…check.

The velocity of money is increasing weekly as the pressure to buy continuously increases due to the continuing devaluation of money one holds…so check again.

The logical conclusion IF the premise expounded is correct is that we are rapidly entering a period of currency collapse. That is NOT to say that currency is now – or will be in the immediate future – however, it does mean that currency will reach a point in the not too distant future where it effectively becomes worthless; think ‘Wiemar Republic’ here. That said, in our financialized World, the first victims of any impending collapse will be Credit Cards, Debit Cards, EBT Cards and the like. As soon as the Majors see the writing on the wall thier first response will be to clamp off the hemorrhaging in the broader system by clamping off unsecured credit.

At THAT point Cash will be King…for a time only. Whether that is a week, a month or a quarter remains a function of the speed of the ongoing collapse; the faster the velocity of the collapse the shorter the window of viability of Cash. After that, the sole options will revolve around PM…which you would be well advised to NOT reveal your ownership of Gold of any sort; use universally recognizeable ‘Junk Silver’ instead. At issue here with Au is that anyone KNOWS you have it, they’ll hunt you down like a dog to take it from you…if necessary, putting your family at gunpoint to force the matter.

The Train has already left the station folks…get ready, it’s going to be a BUMPY ride.

JOG

Never read the article but there should be a marked difference between premodern commodity currency inflation and postmodern fiat currency inflation.

Also, the ZH article as described blithely ignores the necessary third variable in the equation, availability of goods and services.

Classic Weimar inflation was caused by too much fiat printed chasing too few goods and services in an economic downcycle. This reduced velocity of money was resolving as production of goods and services recovered with the economic upcycle.

Wokemodern Bidenflation is the result of artificially reducing the amount of goods and services, which in turn reduces velocity of money.

However, excess currency remains locked up in financial instruments or lost to speculation and so cannot dramatically affect inflation chasing goods and services.

Howdy Brockland,

The distinct difference between commodity currency based inflation and post-modern fiat currency inflation is one of degree, not character, in my considered opinion. In the time when ‘things’ were the basis of trade there was a certain inertia in the whole of the supply chain itself that is wholly absent from everything in our New Brave Financiallized existence.

“FIAT” is fundamentally defined as ‘by command or dictate’ and as such – arbitrarily – any entitled moron can simply declare the value if this or that (especially currency) to be anything they want it to be.

The Law of Supply vs Demand is one of the few laws of existence outside of Physics which simply doesn’t tolerate arbitrary adjustment at all. It’s a tad more ‘elastic’ than the rules of Physics…but whatever you attempt to do with it ends up being principally similar to storing energy in a spring.

In the current timeframe the PTB are using the Logistics system in a way designed to maximize thier profits whilst impoverishing every other part of the economy at large. This is very much by design.

Quite a while ago a gentleman by the name of David Korowicz wrote a paper which can still be found on the Internet titled ‘Tradeoff.pdf’ in which he explored the interconnect between the JIT (Just in Time) Logistics system and the Financial Sphere. It’s quite a read at over 77 pages and careful attention must be paid in the first 30 pages to HOW he uses his terminology but even that limited segment of our modern reality via his analysis shows how remarkably frail our systems have become as Financialization of everything proceeded over the last few decades.

Currently, due to supply chain snafus (entirely engineered, IMHO) you naturally have a reduced amount of goods being chased by rather larger amounts of money due in greatest part to the FED’s printing of vast amounts of currency and releasing that into the broader economy, however, the FED’s primary effort is – and has been since it’s inception – to pad the pockets of it’s cronies and apparatchiks. In a sense, the USA is being led by the nose down the path of Soviet-style Tyranny by the Fed’s actions.

We are NOT experiencing Hyperinflation yet, to be sure…but it will come as the last elements of resiliency in the economy finally capitulate in the face of overwhelming inefficiencies in the rest of the Great Machine. Oh, and your assertion that so much being tied up in various instruments has no bearing on the greater picture: it’s what you have to accomplish with capital on hand daily that defines the trajectory I described originally.

We will soon return to ‘an Age of Things’ where what you HAVE on-hand will define WHAT you are…and your ability to defend it.

Good Luck everyone.

JOG

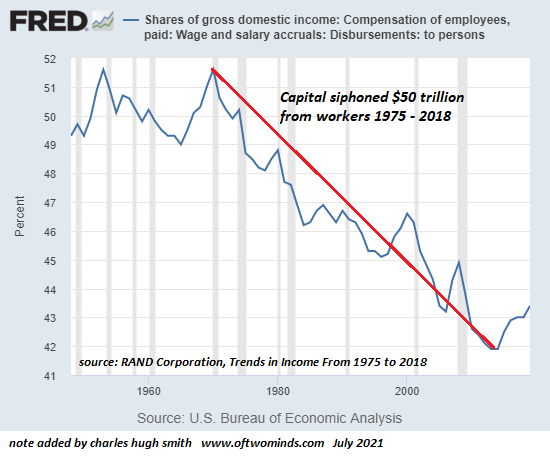

Notice in his chart that labor’s share of GDP began going down in 1975.This was caused by the de-coupling of the currency from precious. It allowed for the rapid expansion of the M2 money/credit supply, going mostly to the MIIC and Wall Street. Labor’s share did not increase as fast under unbacked fiat.

About credit cards. The banks are not too concerned about people not paying them off. Say your limit is set at $10,000. There is no pool of $10,000 laying around waiting for you to spend. The credit is created at the point of your purchase and interest added, same as any loan from a bank. When you pay back the credit, that amount is destroyed…taken out of the system. The banks only care about the interest payments. That is their profit and a tidy one, at that. Compound interest is exponential in growth.

Should you default on a credit card, the bank gets to write that off their books, and then they sell your debt to a collection agency for pennies on the dollar. This is also profit for the bank. So they are not really concerned about repayment. The collection agency will hound you until you pay or take you to court and get a judgement against you. This is also mostly profit.

And all this profit is gained from credit that was created from thin air. Banking is a profitable gig if, you can get it. Funny how bankers are held up as pillars of society when all they do is rob people by way of usury attached to a nebulous creation such as credit.

Economics 101 says that the money supply is created by fractional reserve banking. That is a lie. Deposits are entered as a liability on the books, and your debt/loan is entered as an asset. No deposits are used to make loans. Loans are all created by entering digits into your account whenever the loan is approved. No money is moved around in this transaction. The money supply is created at the point of the loan and usury (profit) added. In order to repay the principal plus compound interest (an exponential function), the amount of loans must be created at an exponential rate. The government jumps in to borrow when the private sector no longer is able. This is why the debt clock spins faster and faster.

The moment the growth of the worldwide credit supply slows down or stops, is the moment of collapse of industrial civilization.

Dr Albert Bartlett, may he rest in peace, said that the biggest shortcoming of the human race was the inability to understand the exponential function.

Like poster “Genius” has said many times before;

Only fools put their money in the bank.

*… Dr. Albert Bartlett was a Malthusian, which should ring alarm bells for anyone logically, morally, and ethically opposed to the Globalist depopulation agenda.

Malthus’ exponential model was probably the first modern mathematical social engineering scam.

Malthusianism lends itself to gaming the Hegelian Dialectic of having a solution in need of a problem.

Everyone intuitively understands the exponential function; stuff runs out. Everyone misunderstands, stuff’s not necessarily running out right NOW.

Its impossible to say if Bartlett was honestly wrong or cleverly lying for an elite faction because everyone including himself appears to misunderstand the exponential function as ‘stuff’s running out right now’.

The Globalists and their enablers aren’t interested in ecological health, just their own wealth and the power gap between themselves and everyone else. Malthusianism provided a believable pretext because everyone does (mis)understand exponentialism.

The exponential function outside strict math contexts is inherently flawed because it assumes linear growth within atomistic parameters rather than cyclical growth within holistic parameters. On the other hand, having that understanding is the foundation of a lot of inside track scamming.

Fractional reserve banking is a legit redundancy in a fiat monetary system where the money supply is fluid by default. Its a way of going beyond mere storage of existing liquid wealth and tapping into future wealth creation.

In commodity currency terms, for example, how many years of grain should be stored against famine?

Fractional reserve banking is only a problem when there is no future wealth to tap into, like going long on buggy whips, then there’s a problem.

Usury does create greater opportunities for corruption, though.

For example, one assumes bankers make loans to profit off the interest, not run scams to seize valuable collateral.

To complete the fractional reserve banking/commodity currency example, how much grain should be stored against famine and for how many years?

Obviously, some amount of grain has to be replanted, eaten, traded, and grain has a shelf life before spoilage destroys value as surely as inflation to fiat under a mattress.